.png?width=410&name=image%20(3).png "image (3)")

We are building a new payment system that will enable tokenised, peer-to-peer markets.

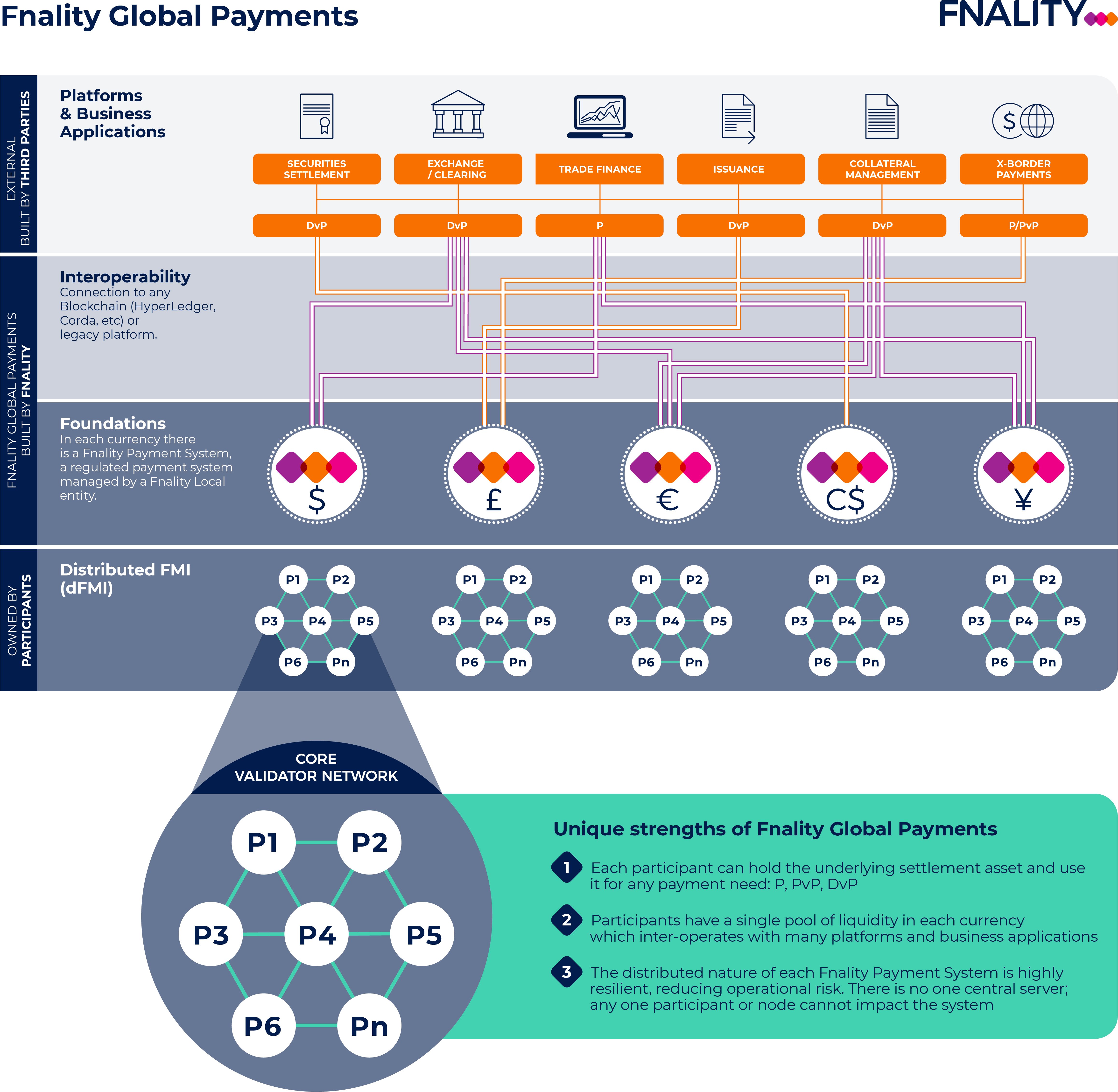

Fnality Global Payments (FnGP) will comprise a series of national systems, each regulated in its home jurisdiction. We call each of these a Fnality Payment System (FnPS)

In each payment system, a Fnality settlement asset will act as the settlement/payment asset for any Payment (P), Delivery v, Payment (DvP) or payment vs. payment (PvP) need.